Aminata Concession Does Not Mean Revenue Loss Or Tax Waiver

Recent commentary surrounding the Aminata & Sons concession agreement currently before Parliament has unfortunately been driven more by speculation than by the actual contents and intent of the agreement.

The first and most important fact is that the agreement does not seek a tax waiver. It seeks a tax deferment for a limited period of three years. There is a significant difference between the two.

A tax waiver permanently exempts a company from paying certain taxes, resulting in the Government foregoing revenue altogether. A tax deferment, on the other hand, simply postpones payment obligations to allow an investor to channel resources into expansion, infrastructure development and operational improvements before meeting those obligations. The revenue is delayed, not lost.

This distinction is critical because the narrative being promoted by critics suggests that Government is giving away revenue. That is simply not the case.

Around the world, governments routinely provide tax deferments, tax holidays and other investment incentives to encourage businesses to undertake major capital investments that create jobs, improve infrastructure and strengthen strategic sectors of the economy. Such incentives are recognised economic tools designed to stimulate growth and ultimately increase government revenue over the long term.

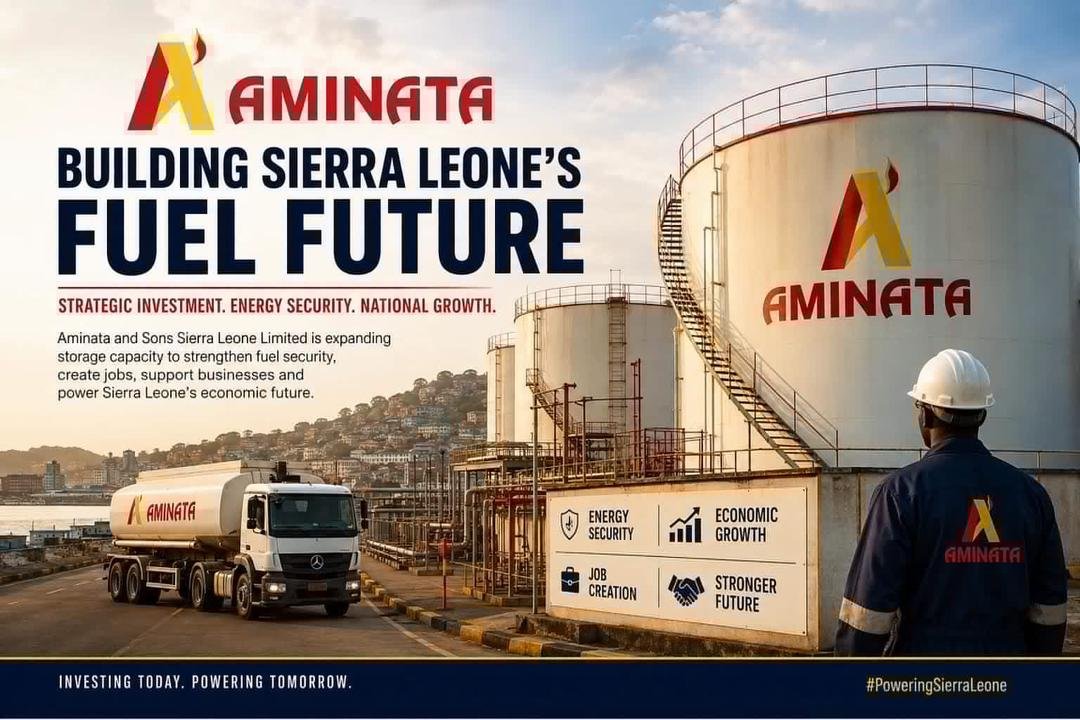

In the case of Aminata & Sons, the company is not a newcomer seeking preferential treatment without a proven record. It has already established itself as a credible and reliable player within Sierra Leone’s petroleum sector. Within a relatively short period, the company has demonstrated its commitment to maintaining high operational standards, ensuring product availability and investing in petroleum infrastructure.

The objective of the proposed deferment is straightforward: enable the company to expand its storage capacity, improve efficiency and strengthen fuel security for the country. These investments require substantial capital expenditure, and the temporary deferment is intended to free up resources for that purpose.

Critics also ignore a fundamental economic reality. Increased storage capacity means greater petroleum reserves, improved supply chain management, reduced vulnerability to shortages, enhanced market stability and greater economic activity. All of these factors ultimately contribute to higher revenue generation for Government through expanded business operations, employment opportunities and increased economic transactions.

Furthermore, comparisons with certain mining agreements are misplaced. Many extractive industry agreements have involved extensive fiscal incentives, exemptions and complex tax arrangements spanning several years. The Aminata & Sons arrangement is far more limited in scope and is focused specifically on supporting infrastructure expansion in a strategic sector that directly affects every Sierra Leonean through fuel availability and pricing.

It is also noteworthy that the proposal received unanimous Cabinet approval. Cabinet’s endorsement suggests that the agreement underwent rigorous scrutiny by the relevant ministries, economic planners and legal experts before being forwarded to Parliament. Such consensus would not have been achieved if the agreement genuinely threatened national revenue interests.

The debate therefore should not be framed around a false narrative of “revenue loss.” The real question is whether Sierra Leone wants indigenous companies with proven track records to expand, invest and strengthen critical national infrastructure.

If the answer is yes, then a temporary tax deferment aimed at increasing storage capacity and operational efficiency should be viewed for what it is: an investment facilitation measure designed to generate greater long-term economic benefits, not a giveaway of public resources.

Parliament’s responsibility should be to assess the agreement on its merits, its economic impact and its contribution to national energy security—not on misconceptions that confuse tax deferment with tax waiver or investment support with revenue loss.